As of 2026, there is no single rule for cryptocurrency in the United States. Instead, each state has its own set of rules - and they don’t match up. If you're running a crypto business, trading, or even just holding digital assets, where you live matters more than you think. Some states make it easy to operate. Others make it so expensive and complicated that companies leave. This isn’t theoretical. It’s real, and it’s changing where money flows, where jobs go, and who gets left behind.

Why State Rules Matter More Than Federal Ones

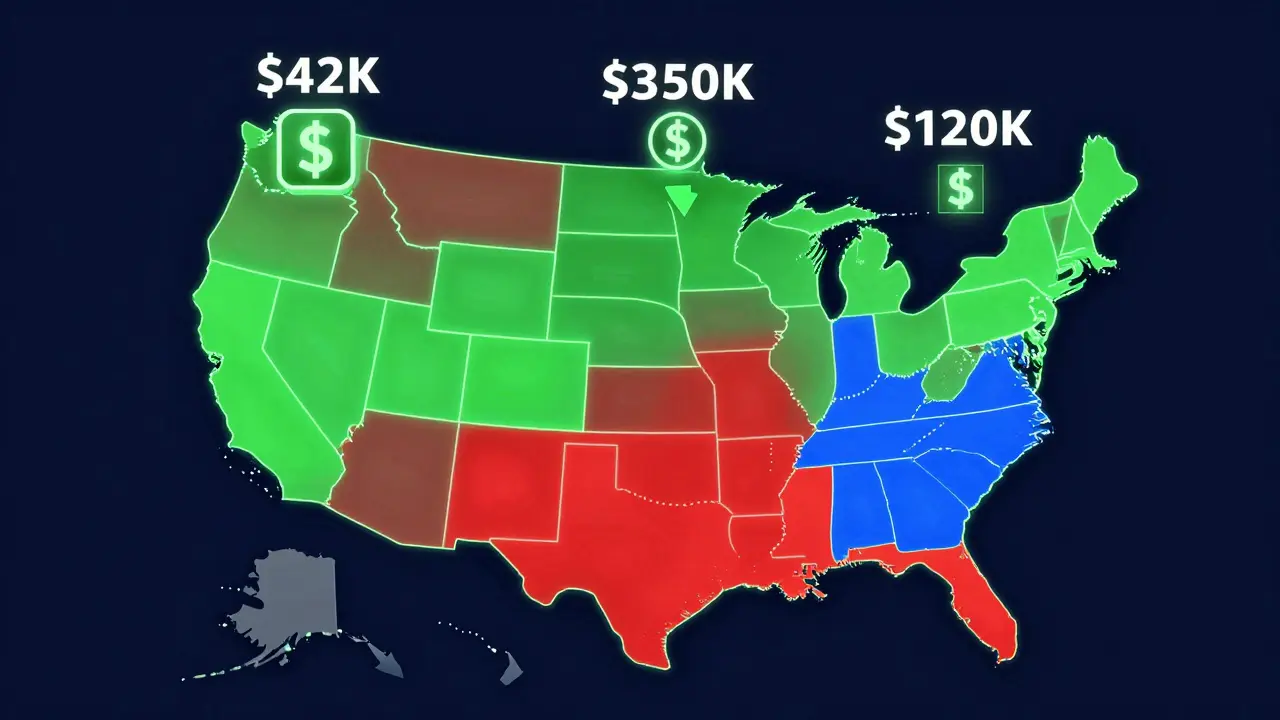

You might assume the federal government sets the rules for crypto. It doesn’t. As of early 2026, the U.S. still lacks a unified national framework. Even after the GENIUS Act passed in September 2025, states still have full power to regulate crypto activities within their borders. That means if you’re a crypto exchange, wallet provider, or even a small business accepting Bitcoin, you could be subject to 47 different sets of rules - each with different fees, reporting requirements, and licensing steps.The result? A patchwork system where compliance costs can jump from $42,000 a year in Wyoming to over $350,000 in New York. That’s not a typo. One state charges less than the cost of a used car. Another charges more than a small business owner makes in a year. And it’s not just about money - it’s about time. Getting a license in New York can take over a year. In California, it takes six weeks.

New York’s BitLicense: The Hardest Path

New York’s BitLicense, created in 2015 by the Department of Financial Services (NYDFS), was the first major attempt to regulate crypto. It’s also the most restrictive. To get licensed, you need:- A $5,000 application fee

- At least $2 million in net capital

- Detailed business plans, anti-money laundering programs, and cybersecurity plans that meet NYDFS 500.00 standards

- 80% of customer assets stored in cold storage with biometric access controls

- Onsite inspections every year

As of September 2025, only 37 companies held active BitLicenses out of 104 applications. Coinbase, Circle, and other major players moved their main operations out of New York. Why? Because the cost and delay weren’t worth it. One exchange founder in Reddit’s r/CryptoCurrency said he spent $187,000 on compliance in NYC - and made zero revenue. He moved to Wyoming and tripled his volume in 18 months.

Users feel it too. New York residents report an average of 217 days to resolve a crypto complaint. Compare that to California’s 38% faster resolution rate. The BitLicense didn’t stop fraud - it just made it harder for honest businesses to operate.

Wyoming: The Crypto-Friendly State

Wyoming flipped the script in 2018 with its Special Purpose Depository Institution (SPDI) law. It didn’t just regulate crypto - it gave crypto companies the legal status of banks. An SPDI can accept crypto deposits, issue loans, and even hold FDIC insurance. That’s huge. It means a crypto firm can operate like a real bank - without being a traditional one.Today, 12 crypto-native banks operate under this law, including Kraken Bank and Avanti Financial Group. In 2024 alone, these institutions processed $12.7 billion in crypto transactions. Wyoming doesn’t just attract companies - it attracts talent. Since 2020, 63% of all new crypto banking jobs in the U.S. have been created in Wyoming.

The cost? You need $25 million in capital and a 6- to 8-month approval process. But for serious players, that’s a bargain. Wyoming’s regulatory fees average $42,000 per year - less than one-tenth of New York’s. And there’s no state income tax. No sales tax on crypto. No capital gains tax. It’s not a gimmick. It’s a strategy - and it’s working.

California: The Middle Ground

California took a different route. Instead of a full license, it uses a registration system under the Department of Financial Protection and Innovation (DFPI). If you’re handling more than $500,000 in crypto transactions annually, you must register. No $2 million capital requirement. No biometric security mandates. Just basic reporting and anti-fraud controls.As of Q3 2025, 142 crypto businesses were registered in California - more than any other state except Texas. The process takes 45 to 60 days. Enforcement is active - 17 actions were taken in 2024 against unregistered firms - but it’s not designed to scare off innovation. It’s designed to catch bad actors.

California’s approach has worked. It’s become a hub for startups, DeFi protocols, and NFT marketplaces. The state’s consumer protection system is also more responsive. Disputes get resolved faster. Users report fewer delays. It’s not perfect - but it’s functional.

Other States: The Wild West

Not every state has a clear system. Some are still figuring it out. Others are actively hostile.- Texas: No license required for most crypto activities. Just basic cybersecurity plans under Finance Code Chapter 152. Minimum bonding: $25,000.

- Louisiana: Exempts businesses doing under $35,000/year in crypto. Above that? A license costing $10,000 and a 6-month review.

- Arizona: Offers a regulatory sandbox. Startups can test products for up to 24 months without full licensing. Result? 34% faster crypto startup growth than non-sandbox states.

- Massachusetts: One of the strictest. Secretary William Galvin called the state-by-state system a "recipe for disaster." Massachusetts recovered $2.1 billion from crypto scams between 2020 and 2025. But critics say its aggressive enforcement scares away legitimate businesses.

Some states require bonding - a financial guarantee that you’ll cover losses if something goes wrong. Others don’t. Some define crypto as a security. Others say it’s a commodity. The lack of alignment creates confusion. A company that’s legal in Nevada might be illegal in New Jersey - even if they’re doing the exact same thing.

What This Means for You

If you’re a business owner:- Consider where you incorporate. Wyoming and South Dakota are top choices for crypto-native firms.

- Don’t assume your New York license covers you in Florida. You need state-by-state compliance.

- Track changes. In 2025 alone, 41 new crypto laws passed across 32 states.

If you’re a trader or holder:

- Your state’s rules may affect how you buy, sell, or report crypto.

- Some states now require crypto transactions to be reported like cash transfers.

- Using a wallet service based in Wyoming or California may mean faster support and fewer freezes.

Even if you’re not in the industry, this matters. The movement of crypto businesses affects local economies. Wyoming’s crypto sector contributed $427 million to state revenue in 2024 - 7.3% of its total income. New York, despite having 10 times the population, only got $189 million - 0.8% of its revenue.

The Future: Federal vs. State

The GENIUS Act of 2025 tried to bring order. It set federal standards for stablecoins and gave the CFTC primary oversight. But 22 states are now suing, claiming it violates their rights under the 10th Amendment. The legal battle isn’t over. It’s just beginning.Experts agree: the current system is unsustainable. A 2025 study from the Wharton Stevens Center found that multi-state operators spend an average of $287,000 a year just on state compliance fees. That’s money not spent on security, innovation, or customer service.

By 2028, we’ll likely see one of two outcomes:

- A federal law that preempts state rules - meaning only one set of rules applies nationwide.

- A formal partnership where states keep authority but agree to standardized rules - like a national template with local tweaks.

Until then, the state you live in still decides how easy or hard crypto will be for you.

Which states have the easiest crypto regulations in 2026?

Wyoming leads with its Special Purpose Depository Institution (SPDI) law, allowing crypto firms to operate as state-chartered banks. California follows with its low-barrier registration system for businesses doing over $500,000/year in crypto. Texas, Tennessee, and Arizona also rank high due to minimal licensing, tax exemptions, or regulatory sandboxes.

Why is New York’s BitLicense so strict?

New York created the BitLicense in 2015 as a response to high-profile crypto frauds and money laundering risks. The goal was consumer protection - but the requirements became so heavy that even major firms like Coinbase left. The state requires $2 million in capital, 80% cold storage, biometric security, and annual onsite exams. The result? Only 37 active licenses out of 104 applications as of 2025.

Can I operate a crypto business in multiple states?

Yes - but it’s expensive. Most companies must register or license in each state where they have customers or employees. Compliance costs average $287,000 per year for multi-state operators. Many choose to base operations in one friendly state (like Wyoming) and limit their customer base to avoid complex licensing.

Do I need to report crypto transactions to my state?

It depends. States like New York and Massachusetts require reporting for businesses and sometimes individuals. California requires reporting only for businesses over $500,000/year. Most states don’t require individual reporting yet - but that’s changing. Always check your state’s Department of Financial Services or equivalent agency.

What’s the difference between a license and a registration?

A license (like New York’s BitLicense) is a full approval with high costs, capital requirements, and ongoing exams. A registration (like California’s) is simpler - you submit basic info and pay a fee, but there’s no capital requirement or in-person inspection. Registration is faster and cheaper, but still legally binding.

Will federal law override state rules soon?

The GENIUS Act of 2025 set federal standards for stablecoins and gave the CFTC primary oversight. But 22 states are challenging it in court, arguing it violates state sovereignty. A full federal takeover is unlikely before 2028. More likely: a hybrid system where federal rules set minimum standards, but states keep authority over local enforcement and taxation.

How do state rules affect crypto taxes?

State tax rules vary. Wyoming, Nevada, and Texas have no state income tax - so crypto gains aren’t taxed at the state level. California taxes crypto as income, like wages. New York treats crypto sales as capital gains. Always check your state’s tax agency - crypto tax rules are separate from federal IRS rules and often overlooked.

Author

Ronan Caverly

I'm a blockchain analyst and market strategist bridging crypto and equities. I research protocols, decode tokenomics, and track exchange flows to spot risk and opportunity. I invest privately and advise fintech teams on go-to-market and compliance-aware growth. I also publish weekly insights to help retail and funds navigate digital asset cycles.