Buying a cryptocurrency with the name INSURANCE feels like a trap. It sounds safe, but in the world of decentralized finance, names often hide danger rather than prevent it. If you are looking at the INSURANCE token on your screen right now, you need to understand exactly what you are holding before you click "swap." This isn't just another meme coin; it is a high-risk asset on the BNB Chain with specific technical flaws that could wipe out your funds.

As of May 2026, the INSURANCE token trades with extreme volatility and significant centralization risks. While the price has seen massive swings-ranging from an all-time low of $2.16 to a peak of $78.72-the underlying technology contains features that give developers total control over your money. Understanding these mechanics is crucial for anyone considering this investment.

Key Takeaways: The Reality of INSURANCE Token

- INSURANCE Token operates on the BNB Chain ecosystem as a speculative asset with limited liquidity.

- The smart contract includes dangerous features like self-destruct capabilities and centralized minting rights for developers.

- Current market data shows high volatility, with prices fluctuating wildly between exchanges due to low trading volume.

- The token ranks outside the top 14,000 cryptocurrencies by market cap, indicating it is an early-stage or niche project.

- There is no clear utility or whitepaper linking the token to actual insurance services, making it primarily a speculative trade.

What Is the INSURANCE (INSURANCE) Crypto Coin?

At its core, INSURANCE is a cryptocurrency token built on the BNB Chain blockchain. Unlike traditional insurance products that protect against car accidents or health issues, this token does not appear to offer any tangible coverage. Instead, it functions as a digital asset traded on decentralized exchanges (DEXs).

The token uses the ticker symbol INSURANCE and interacts with wallets like MetaMask via the contract address 0x64e4fea6e4f3637025c7bcd878e2b238b01f7d4e. When you buy this token, you are essentially betting on its price movement within the BNB Chain ecosystem. There is no evidence of a functional insurance protocol behind it. Most tokens in this category rely on community hype or speculative trading rather than real-world utility.

If you are new to crypto, you might assume the name implies safety. In reality, the intersection of blockchain and insurance is a complex field involving smart contracts for claims processing and identity verification. The INSURANCE token seems to ride the coattails of this buzzword without delivering the technology. Always check if a project has a working product before assuming its name reflects its function.

Tokenomics: Supply, Valuation, and Market Cap

Understanding the supply dynamics helps explain why the price moves so erratically. The INSURANCE token has a fixed maximum supply of 100,000,000 coins. Currently, approximately 98,000,000 coins are in circulation. This means only 2% of the total supply remains unissued, which might sound stable, but the risk lies in how those remaining tokens are handled.

| Attribute | Value / Detail |

|---|---|

| Total Max Supply | 100,000,000 INSURANCE |

| Circulating Supply | ~98,000,000 INSURANCE |

| Blockchain Network | BNB Chain (BSC) |

| Contract Address | 0x64e4fea6e4f3637025c7bcd878e2b238b01f7d4e |

| Fully Diluted Valuation (FDV) | BTC 64,446.43 (approx.) |

| Market Rank | #14,063+ (Low Liquidity) |

The Fully Diluted Valuation (FDV) is calculated based on the assumption that all 100 million tokens are active. An FDV represented in Bitcoin terms (BTC 64,446) suggests a theoretical market cap that is difficult to sustain given the low trading volume. Low liquidity means that large sell orders can crash the price instantly. You might see a price of $300 on one exchange and $280 on another because there aren't enough buyers to stabilize the rate.

Price History and Volatility Analysis

The price action of INSURANCE is a textbook example of high-risk speculation. Let's look at the numbers. On October 29, 2024, the token hit an all-time low of just $2.16. Fast forward to July 24, 2025, and it surged to an all-time high of $78.72. That is a 3,499% increase in less than ten months.

Such explosive growth usually attracts attention, but it also creates a fragile foundation. As of mid-2026, the token trades around the $300-$320 range, showing signs of instability. Recent data indicates a 7-day price increase of 7.30%, outperforming the broader crypto market which was down slightly. However, this performance is driven by thin order books. A single large seller dumping their holdings could drop the price by 20% or more in minutes.

Trading volume is another red flag. The 24-hour volume hovers between $62,000 and $171,000 USD. For a token priced at hundreds of dollars per unit, this volume is incredibly low. It means you cannot easily enter or exit positions without affecting the price significantly. If you buy $1,000 worth, you might be buying a large percentage of the day's available supply.

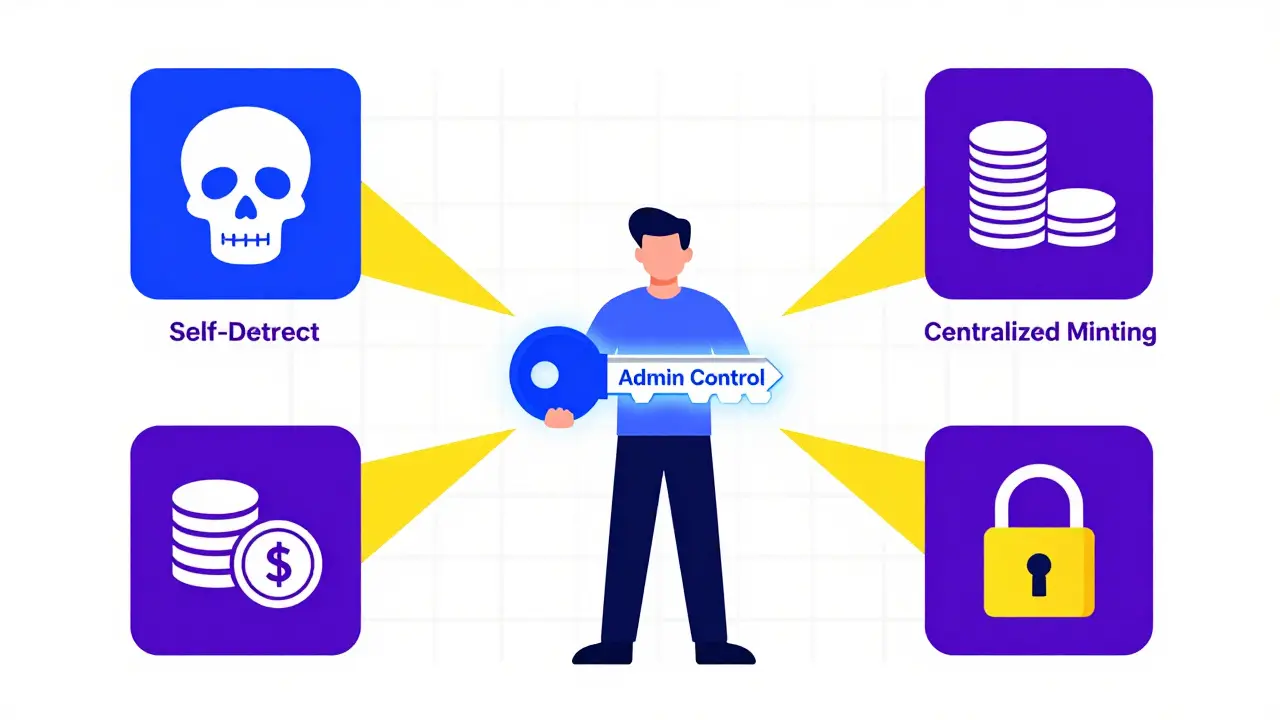

Critical Smart Contract Risks: Why This Token Is Dangerous

This is the most important section for your wallet's safety. Many investors look at price charts and ignore the code. For INSURANCE, the code reveals severe vulnerabilities. According to risk analyses from platforms like CoinStats, the smart contract has several "centralized" features that contradict the ethos of decentralization.

- Centralized Minting: The developers retain the ability to create new tokens at any time. If they decide to mint millions more INSURANCE tokens, the value of your existing holdings will dilute instantly. You have no say in this process.

- Self-Destruct Functionality: The contract includes a command that allows the creator to delete the entire contract. If triggered, all tokens held in that contract-and potentially associated liquidity pools-could become worthless. This is a common feature in scam tokens designed to rug-pull investors.

- Wallet Blocking: Developers can blacklist specific addresses. This means they can stop you from selling your tokens if they choose to. You might own the asset, but you cannot move it.

- Proxy Contracts (Upgradability): The token uses a proxy design, meaning the rules can be changed after launch. Today, the tax on sales might be 0%. Tomorrow, the developer could update the code to charge a 50% tax on every transaction. Your money stays in the contract, not your wallet.

These features indicate that you do not truly own the token. You are holding a permissioned asset where the creators hold the master keys. In a healthy decentralized project, these functions are renounced or locked permanently. With INSURANCE, they remain active.

Where to Trade: Exchanges and Liquidity Pools

You won't find INSURANCE on major centralized exchanges like Coinbase or Binance. It trades exclusively on decentralized exchanges (DEXs) within the BNB Chain ecosystem. The primary venues include:

- ApeSwap: Trades the INSURANCE/MGC pair. This pool accounts for about 5% of the daily volume. The bid-ask spread here is around 0.6%, which is moderate but can widen during volatility.

- PancakeSwap v2: Hosts multiple pairs, including INSURANCE/unspecified and CAKE/INSURANCE. PancakeSwap handles roughly 7.5% of the volume. The CAKE pair shows extremely low activity (0.1%), suggesting illiquidity in stablecoin or major token pairs.

When trading on these platforms, you must connect your wallet directly to the site. Ensure you are using the correct contract address. Scammers often create fake tokens with the same name but different addresses. Always verify the address 0x64e4fea6e4f3637025c7bcd878e2b238b01f7d4e on a trusted block explorer before connecting.

The Broader Context: Blockchain Insurance vs. Speculative Tokens

To understand why INSURANCE stands out negatively, we must look at what legitimate blockchain insurance looks like. The broader blockchain-insurance sector includes projects focused on parametric insurance, where payouts are triggered automatically by verified data (like flight delays or crop failure). These projects use smart contracts to automate claims without human intervention.

Legitimate protocols in this space typically have:

- Audited smart contracts with no admin privileges.

- Transparent governance models where holders vote on changes.

- Reserve funds backed by diversified assets to pay out claims.

INSURANCE lacks these characteristics. It sits in a market segment of nine known blockchain-based insurance assets with a combined market cap of $5.92 billion. INSURANCE represents a tiny fraction of this. Without a whitepaper detailing its role in this ecosystem, it appears to be a speculative play rather than a functional part of the insurance infrastructure.

Conclusion: Should You Buy INSURANCE?

The decision to invest in INSURANCE comes down to your risk tolerance. If you are seeking exposure to the concept of decentralized insurance, there are safer, more established protocols with audited code and transparent teams. If you are purely speculating on short-term price movements, be aware that the smart contract risks are exceptionally high.

The combination of self-destruct capabilities, centralized minting, and low liquidity makes this token a potential minefield. The price may go up, but the possibility of a sudden collapse due to developer action is real. Never invest more than you can afford to lose entirely. Treat this as a lottery ticket, not an investment.

Is the INSURANCE token a scam?

While not definitively labeled a scam by regulatory bodies, the INSURANCE token exhibits many hallmarks of high-risk or fraudulent projects. Features like the self-destruct function, centralized minting, and the ability for developers to block wallets are common in scams. The lack of a clear utility or team disclosure further increases suspicion.

Which blockchain is INSURANCE token on?

The INSURANCE token operates on the BNB Chain (formerly Binance Smart Chain). This means you need a wallet compatible with BSC, such as MetaMask or Trust Wallet, and some BNB tokens to pay for gas fees when trading.

What is the contract address for INSURANCE?

The verified contract address for the INSURANCE token is 0x64e4fea6e4f3637025c7bcd878e2b238b01f7d4e. Always double-check this address on a block explorer like BscScan to avoid phishing sites.

Why is the price of INSURANCE so volatile?

Volatility is driven by low liquidity and low trading volume. With only tens of thousands of dollars in daily volume, small buy or sell orders can cause large price swings. Additionally, the fear of developer actions (like minting more tokens) contributes to price instability.

Can I buy INSURANCE on Coinbase or Binance?

No, INSURANCE is not listed on major centralized exchanges like Coinbase or Binance. It is only available on decentralized exchanges (DEXs) such as PancakeSwap and ApeSwap within the BNB Chain ecosystem.

What does the self-destruct feature mean for my funds?

If the developer triggers the self-destruct function, the smart contract is deleted from the blockchain. Any tokens held in that contract or associated liquidity pools could become inaccessible or worthless, resulting in a total loss of funds for holders.

How much of the INSURANCE supply is in circulation?

Approximately 98,000,000 out of the 100,000,000 maximum supply tokens are currently in circulation. However, because the contract allows for centralized minting, this number could theoretically change if developers create more tokens.

Is there a whitepaper for the INSURANCE project?

Publicly available research does not indicate the existence of a detailed whitepaper or technical documentation for the INSURANCE token. This lack of transparency is a significant red flag for potential investors.

Author

Ronan Caverly

I'm a blockchain analyst and market strategist bridging crypto and equities. I research protocols, decode tokenomics, and track exchange flows to spot risk and opportunity. I invest privately and advise fintech teams on go-to-market and compliance-aware growth. I also publish weekly insights to help retail and funds navigate digital asset cycles.