JPYC Transaction Fee Calculator

How This Calculator Works

This calculator shows the real value of your JPYC after blockchain transaction fees. Since JPYC runs on multiple blockchains with varying gas costs, you'll see how much your purchase is actually worth after fees.

Note: JPYC's value fluctuates between exchanges. Typical values: Coinbase $0.0067, CoinGecko $0.0072, Kriptomat €0.0076.

Transaction Summary

Chain Comparison:

| Blockchain | Gas Fee | Real Value (USD) | Real Value (JPY) |

|---|---|---|---|

| Ethereum | $1.20 | ||

| Polygon | <$0.01 | ||

| Avalanche | $0.05 | ||

| Gnosis | $0.03 | ||

| Astar | $0.02 | ||

| Shiden | $0.01 |

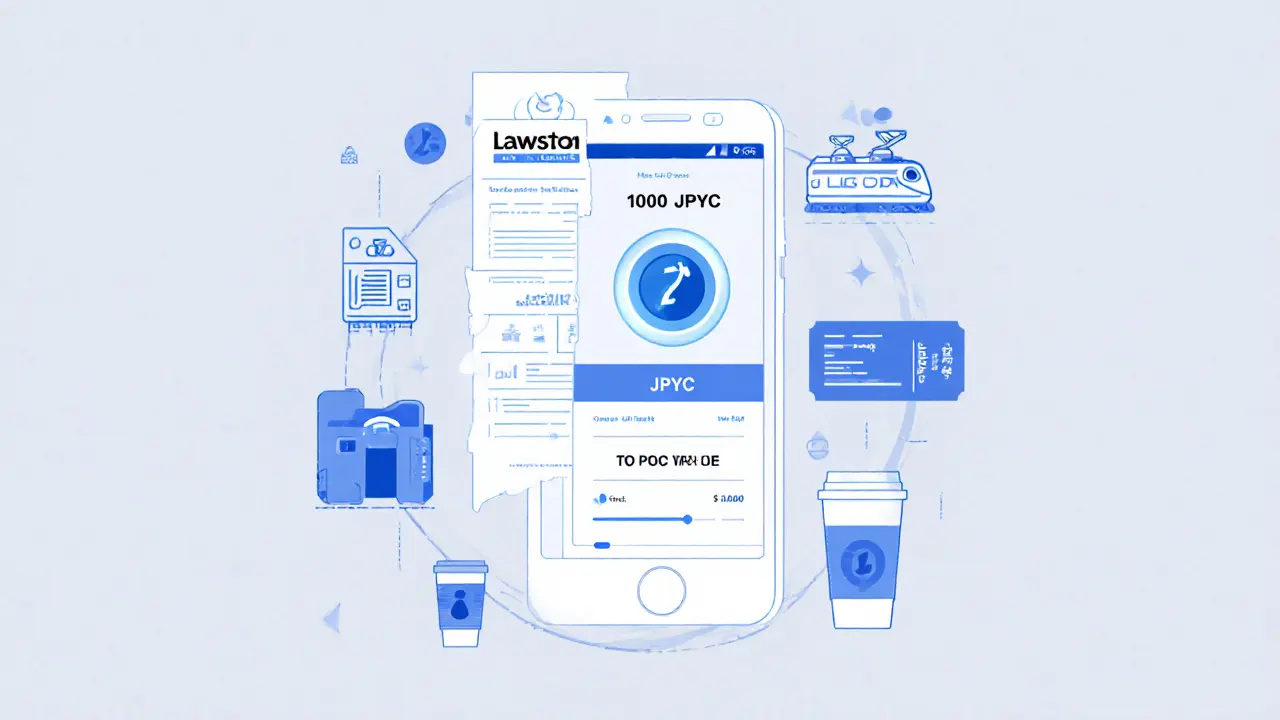

JPY Coin v1, or JPYC, isn’t another speculative crypto coin. It doesn’t promise to make you rich overnight. It doesn’t even act like Bitcoin or Ethereum. Instead, JPYC was built for one simple reason: to let people in Japan use digital money that stays worth exactly what a Japanese yen is worth. That’s it. No hype. No moon shots. Just a digital version of cash that you can hold on your phone and spend at convenience stores.

It’s Not a Crypto, It’s a Prepaid Gift Card

The Japanese Financial Services Agency (FSA) doesn’t classify JPYC as a cryptocurrency. It’s legally a prepaid payment instrument. That means it works more like a V Preca gift card than a Bitcoin. You load it with yen value, and you use it to buy things - not trade it. Think of it like buying a $50 Starbucks gift card. You don’t expect the $50 to turn into $75. You just want to use it for coffee. JPYC is the same. One JPYC token = one Japanese yen. At least, that’s the idea. But here’s the twist: even though it’s supposed to be stable, its price on exchanges keeps swinging. On November 25, 2023, Coinbase showed JPYC trading at $0.0067. CoinGecko showed $0.0072. Kriptomat.io had it at €0.0076. That’s a 25% difference across just three platforms. If it’s supposed to be pegged to the yen, why does its dollar value jump around like a stock? The answer? Because it’s not backed by actual yen reserves in a bank. There’s no public audit. No proof that someone holds 400 million yen to back the 400 million JPYC tokens in circulation. Instead, it relies on a system where users can convert JPYC into V Preca gift cards - which are real, physical cards you can use at Lawson, FamilyMart, and other stores. That’s the only real guarantee: if you can turn JPYC into a gift card that works at a store, then it has value.How JPYC Works: Multi-Chain, But Messy

JPYC runs on six different blockchains: Ethereum, Polygon, Avalanche, Gnosis, Astar, and Shiden. That sounds impressive - until you realize how messy it gets. On Ethereum, gas fees for sending JPYC can hit $1.20 per transaction. On Polygon? Less than a penny. So if you’re trying to send JPYC to pay for a $5 coffee, you’re paying more in fees than the coffee costs. That’s not practical. And because each chain has its own market, prices don’t match up. A JPYC token on Ethereum might trade at $0.007, while the same token on Polygon trades at $0.0063. That’s not stability. That’s fragmentation. Most people who use JPYC aren’t trading it. They’re converting it to V Preca gift cards. That’s the real use case. You buy JPYC on an exchange, send it to your wallet, then swap it for a gift card that works at 1,247 Japanese retailers. It’s a bridge between crypto and cash - but only if you’re in Japan.Why JPYC Isn’t Like USDT or USDC

Tether’s USDT and Circle’s USDC are the giants of stablecoins. They’re backed by cash, bonds, and other assets. They’re audited. They trade billions every day. USDT alone moves over $20 billion in 24 hours. JPYC? $37.41. That’s not a typo. $37.41. That’s less than the price of a single Bitcoin. JPYC trades on only four exchanges. USDT trades on hundreds. USDC is accepted everywhere. JPYC? Mostly in Japan. Even worse, JPYC’s all-time high was $0.0114. As of late November 2023, it was trading at around $0.007 - down 41%. That’s not a stablecoin. That’s a volatile asset pretending to be stable. Experts like Dr. Kenji Sato from Keio University say JPYC’s lack of reserve transparency makes it risky for anything beyond small retail use. If the team behind JPYC disappears tomorrow, there’s no guarantee you can get your yen back.

Who Uses JPYC - And Why

You won’t find hedge funds holding JPYC. You won’t see institutional investors using it. But you will find Japanese small business owners, students, and remittance users. On Reddit, users report using JPYC to send money to Singapore with fees as low as 0.8%. Traditional banks charge 4.2%. That’s a big difference. In Japan, 68% of positive reviews mention using JPYC to buy groceries, snacks, or train tickets via V Preca gift cards. A user named TokyoTrader88 said he uses it to pay for lunch at Lawson every day. Another user, SapporoCrypto, complained it took three days to convert 50,000 JPYC to a gift card - but still used it because there was no better option. JPYC’s real value isn’t in speculation. It’s in accessibility. For people who don’t have bank accounts or hate wire transfers, JPYC offers a way to get yen into digital form - and then into real goods.The Future: CBDCs and Regulatory Risk

Japan is working on its own central bank digital currency (CBDC). The Bank of Japan is testing it. If that launches, JPYC could become obsolete overnight. The FSA is also preparing new rules for stablecoins. Expected in early 2024, the Stablecoin Regulation Bill could require full reserve backing - meaning JPYC’s current prepaid model might not pass. If that happens, JPYC’s team would have to either change how it works - or shut down. Right now, it operates in a gray zone. It’s not illegal. But it’s not fully protected either. On the bright side, JPYC is growing. Merchant adoption rose 18.7% in October 2023 after FamilyMart started accepting V Preca cards. Monthly user growth is at 12%. It’s not massive - but it’s real.

Author

Ronan Caverly

I'm a blockchain analyst and market strategist bridging crypto and equities. I research protocols, decode tokenomics, and track exchange flows to spot risk and opportunity. I invest privately and advise fintech teams on go-to-market and compliance-aware growth. I also publish weekly insights to help retail and funds navigate digital asset cycles.